If you want to search Cost Curve back issues or link to anything you read here, the web links and archive are online at costcurve.beehiiv.com. You can subscribe there, too.

Reminder: Cost Curve is off until Tuesday. Behave, please.

A second appeals court has ruled, unanimously, that pharmaceutical companies can place restrictions on how they deal with contract pharmacies. The D.C. Circuit decision, which involved Novartis and United Therapeutics, isn’t that long, so if you’re into the issue, it’s worth taking the 15 minutes to read.

If you’re rushed, Bloomberg Law and Courthouse News Service have you covered.

The court was pretty clear that HHS can’t demand that pharma companies ship 340B products anywhere, anytime, for any reason, with no ability to negotiate the details. And they were also clear that pharma companies can’t make up their own arbitrary rules, either.

But for the specific pharma restrictions at the center of the suit -- demanding additional documentation or dealing only with a single contract pharmacy -- the court was OK with the way manufacturers are behaving.

This isn’t the final word. States are imposing their own rules dictating how pharma companies deal with contract pharmacies, and the results there haven’t necessarily gone industry’s way. And there is one other appellate court yet to rule on the issue, and a win for the government would make this ripe for Supreme Court consideration.

And, of course, the whole 340B program remains a mess. No one is quite sure how its helping patients, but everyone is quite certain that 340B sales are bonkers.

* A side note: HHS, in its original advisory opinion telling companies that limits on contract pharmacies were not allowed, had kind of a jerk vibe. The opinion bragged that covered entities could demand deliveries to “the lunar surface [or] low-earth orbit.” I’m sure that was fun to write, but the decision included a couple of snide remarks about HHS’ interstellar demands, which makes me wonder if the hyperbolic flourish here didn’t backfire a bit.

I’ve been musing lately that maybe the insulin price/cost thing is mostly solved.

I say “mostly,” because the United States has a very weird and inefficient health care system, and it is very difficult to plug all of the possible holes that a patient might fall through.

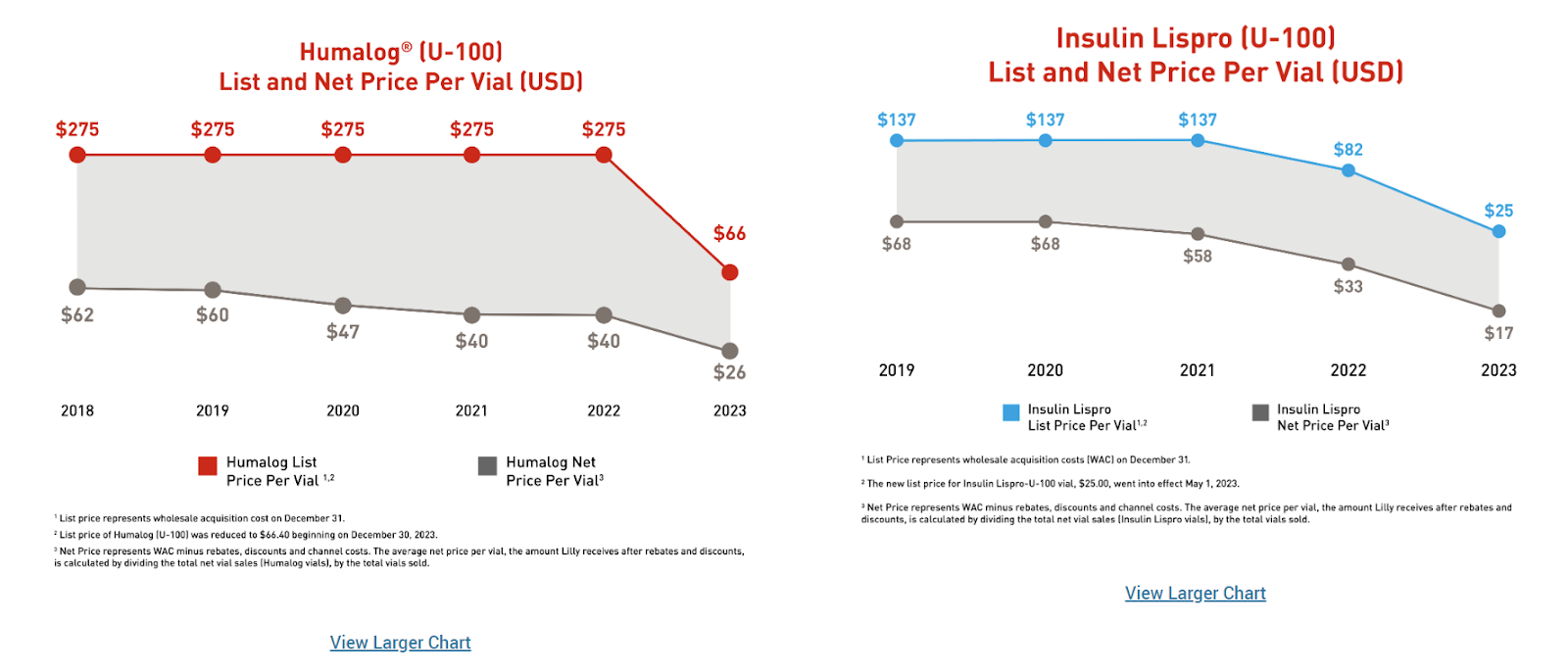

But it seems like the insulin market has come to a point where insulin prices are now so low that access ought not be an issue. The latest evidence of this is the U.S. Access and Affordability section of Lilly’s very good Sustainability Report*, which includes an extended discussion of price, including an incredible amount of detail on insulin pricing.

Per the report, Lilly’s workhorse insulin -- Humalog -- now carries a net price of $26 a vial. Lilly also makes a biosimilar version of the same molecule, which has a net price of $17 a vial. This is, give or take, what payers are paying. It’s not a lot. Patients, on average, are paying about $5 a vial for brand-name Humalog and $3.40 for the biosimilar. Here’s how Lilly’s visualized it:

To put this in context, California has been talking for years about manufacturing its own insulin and charging no more than $30 a vial. (In the end, rather than making the stuff itself, it decided just to pay CivicaRx $50 million to do the manufacturing, though Civica hasn’t yet won FDA approval for its version.)

In other words, the insulin market has shifted so much that even a much-ballyhooed low-price strategy looks like it won’t deliver any savings by the time it’s implemented. I don’t want to suggest that California’s four-year odyssey here was a fool’s errand, only that circumstances on the ground are prone to shift, especially in areas of high competition.

But the policy discussions remain mired in an outdated idea of where the market is, which is why insulin still seems so appealing to politicians. Manufacturers and payers have moved on. Is it time for everyone else to do the same?

* The report (and the accompanying spreadsheet) is where list and net price changes are usually disclosed. Weirdly, Lilly is only disclosing list price changes this year (list prices are up 5%, on average), not net price changes.** It used to present both figures. Lilly does note that net prices are, on average, 34% of list prices, which does tell the net price story in a fairly compelling way.

** Pfizer does the opposite: it gives an average net price change, not an average list price change. Novartis used to report both metrics and now discloses neither.

Maryland’s PDAB has announced the first five drugs it will start to investigate as candidates for price controls. In some ways, it is a weird list. (In fairness, I find all of these PDAB decisions weird, because there are basically no standards for how they’re picking meds.)

They’re going after four diabetes medicines -- Ozempic, Trulicity, Jardiance, and Fargixa -- plus Skyrizi. They’ll apparently tackle Dupixent at some point in the future.

So why is this weird? Well, one of the medicines will be generic in the next three years or so. And three others will have IRA-set prices in the next three years. I mean, maybe this is useful if Maryland is trying to align with IRA prices, but we’re talking about some heavily, heavily rebated drugs, so there may not be much juice to squeeze.

It’s not hard to see shades of the California insulin push here, where a slow-moving bureaucracy is forever a half-step behind the market.

The Senate Judiciary Committee hearing on patents received more coverage than I would have expected (NBC, the lead in Axios Vitals, etc.), mostly because it didn’t advance much. My big question around IP issues is “where is the problem right now?” There are not a lot of medicines with super-long exclusivity at present. Indeed, the biggest issue is probably PBMs suffocating biosimilars (which did come up in the testimony from PhRMA’s Jocelyn Ulrich). Everything else seems to focused on yesterday’s issues.

The single biggest unanswered question around the IRA is “will PBMs play games to restrict access?” We’ve talked about that a lot around here, but we can/should/will talk about it a lot more. With that as prologue: it’s worth watching Adam Fein’s video explainer on how this could all go sideways. Remember, CMS has been pushed to address this, and they’ve continually sidestepped the issue.

Header image via Flickr user Carl Revell.

Thanks for reading this far. I’d be flattered if you shared all or part of Cost Curve. All I ask is for a mention or tag. Bonus points if you can direct someone to the subscription page.