I really tried to make it a whole newsletter without mentioning 340B. I came close, but — alas — I can’t get away.

If you want to search Cost Curve back issues or link to anything you read here, the web links and archive are online at costcurve.beehiiv.com. You can subscribe there, too.

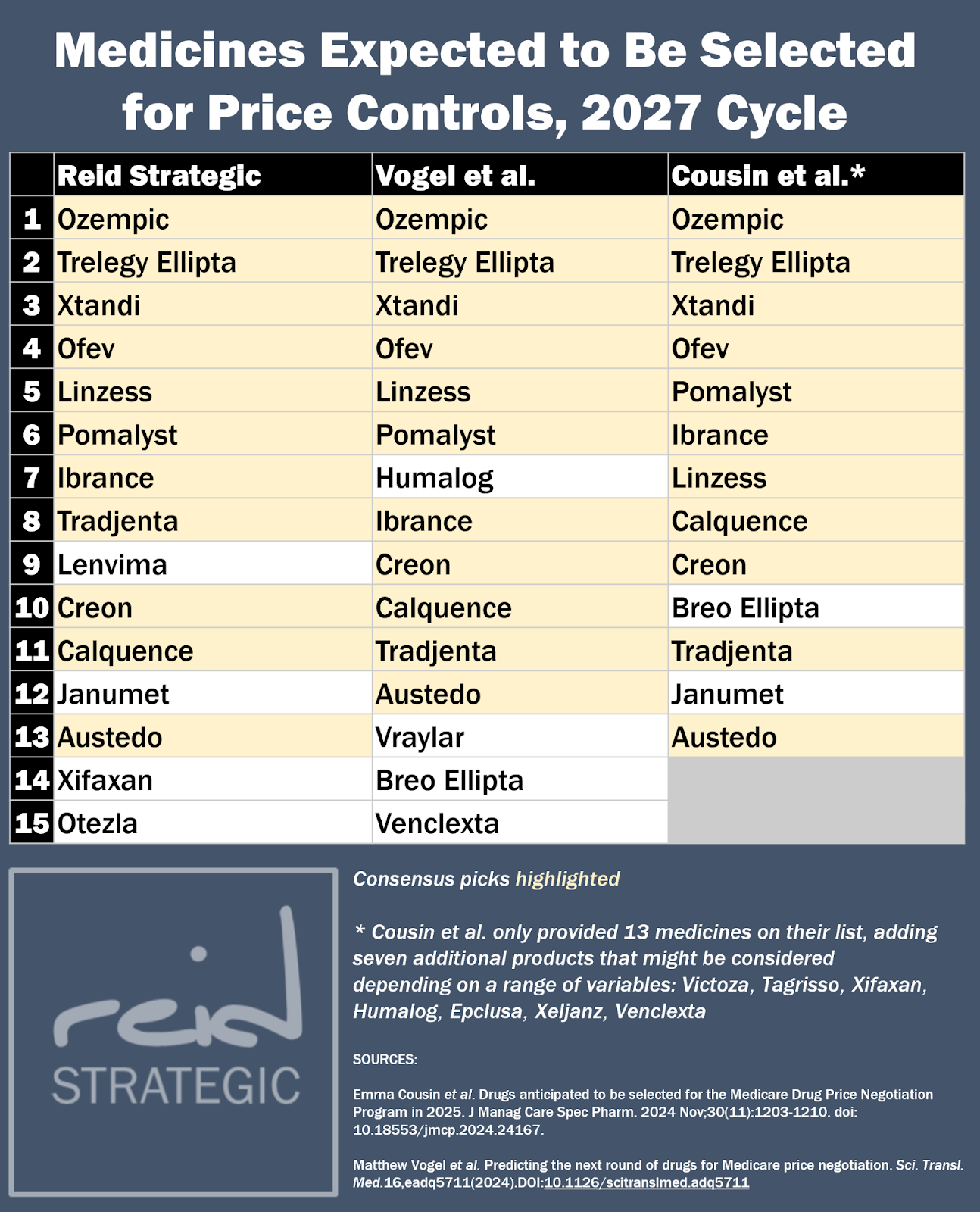

At some point in the next two months**, CMS is going to come out with the next 15 medicines up for “negotiation”/price controls in Medicare.

In some ways, there’s not much drama about how the announcement will go. At the top of the list will be semaglutide -- perhaps you’ve heard of Ozempic and Wegovy? -- so that’s the headline right there. I would assume there will be some legal action about the inclusion of Wegovy,*** too, which is only going to add fuel to that fire.

Still, understanding the other 14 medicines is not unimportant, and -- as noted last week -- we now have two peer-reviewed publications (Cousin and Vogel) estimating which meds will be included. Here are those two lists, along with my ever-changing best-guesses:

The differences between the three lists mostly come down to uncertainty over which medicines have the largest gross Medicare spending. CMS will be looking at sales data that runs from Nov. 1, 2023 to Oct. 31, 2024, but the public only has access to data for calendar year 2022.

How much drug sales changed between 2022 and 2024, then, becomes the key question, and that’s where the inconsistency arises. A few notes:

The Vogel paper includes Humalog, but the price on that medicine was slashed by 70% after the 2022 data dump. Even though the net price probably didn’t change, the gross spending almost certainly nosedived. I think that’s a safe scratch.

Vogel et al also misses Janumet. I suspect that’s because they didn’t account for both plain-vanilla Janumet and its extended release form, which are considered together under the law. (I missed that in my earlier guesses.)

The Cousins paper omits Xifaxan because it’s Salix’s primary drug (which is an exclusion under the IRA), but Salix is wholly owned by Bausch, so it’s probably eligible. (Vogel has Xifaxan on the bubble due to sales.)

If I had to choose one of my picks to be nervous about it, it’s Breo. My assumption is that even though that drug had pretty strong 2022 sales in Medicare, growth has been fairly flat in the United States as patients shift to news meds. But that’s the kind of uncertainty that’s appearing at the margins.

Even though the story here is going to be on Ozempic, the potential for impact is going to stretch all the way down the list. If you’re a company that hasn’t yet fully prepared for the 2027 process, it’s not too late. Just drop me a line.

** Technically, the announcement is due by Feb. 1. But the first 10 medicines were announced ahead of the statutory deadline, and there is a general assumption -- unencumbered by any actual facts -- that the Biden administration will want to manage the reveal before Trump 2.0 begins on January 20.

*** Part of the existing legal argument being made by Novo Nordisk is the CMS can’t just smoosh together drugs that have the same ingredient for the purposes of the IRA. It might be the same molecule, but it’s treated entirely differently by the FDA, etc., and the company thinking is that there’s no reason why this law should deviate from that standard.

There’s less chatter than I would have expected out of the Supreme Court decision not to hear the state-level 340B contract pharmacy dispute, handing a win to the states. Reuters has coverage, and Arkansas officials generated some hometown stories, but otherwise: kind of quiet.

Vertex’s non-opioid pain drug won a quiet but convincing endorsement from ICER, which said that the medicine would be cost-saving at a placeholder price of $420 per course. The savings mostly come via the prevention of opioid abuse. Still, the group sounded alarms about budget impact, and I have no idea how accurate that placeholder price will be.

Bernie Sanders has a PBM bill, and CBO just scored it as costing the government money. (Other bills are cost-savings.) As one wag giggled this morning: “Sanders would have the one PBM bill that costs money…”

Bruce Japsen over at Forbes has some details on Blue Shield of California’s big plan to live (mostly) without a big-three PBM. That effort will launch next months and, tbh, I feel like we should have heard a lot more about this deal.

BIO.News is producing some solid PBM content, trying to look at reform efforts through the impact on patients, going issue by issue. Here’s one on transparency, one on rebate pass-through, one on pharmacies on the brink, one on delinkage, and one on step therapy.

When biopharma CEOs speak, it’s worth listening. Here is Ultragenyx CEO Emil Kakkis in BioSpace making the point that accelerated approval is indeed delivering better meds more quickly (and making a strong pro-biomarker argument, too).

Cost Curve is produced by Reid Strategic, a consultancy that helps companies and organizations in life sciences communicate more clearly and more loudly about issues of value, access, and pricing. We offer a range of services, from strategic planning to tactical execution, designed to shatter the complexity that hampers constructive conversations.

To learn more about how Reid Strategic can help you, email Brian Reid at [email protected].